“Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn't, pays it.” -- Albert Einstein

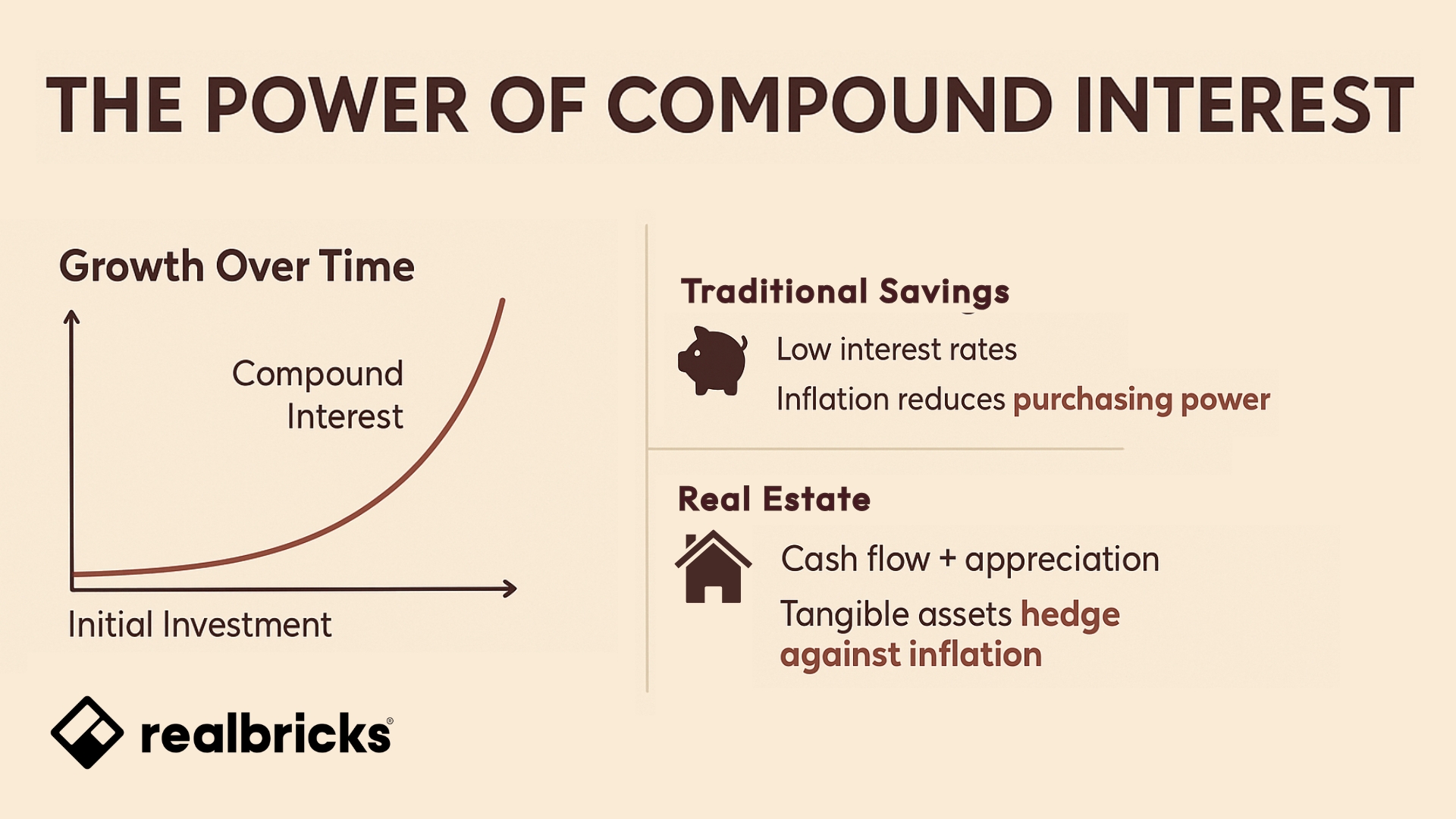

When it comes to building long-term wealth, few concepts are as quietly powerful as compound interest. It’s the process of earning returns on both your original investment and the growth that follows — a snowball effect that turns small beginnings into substantial gains over time.

At its core, compound interest means your money works for you — and then your returns start working too.

For example, if you invest $1,000 at a 10% annual return, you’ll have $1,100 after the first year. In year two, you earn interest on $1,100 — not just the original $1,000 — and the effect compounds year after year.

Over decades, this exponential curve creates what Einstein reportedly called “the eighth wonder of the world.” But not all investments compound equally.

Traditional accounts like savings accounts and certificates of deposit (CDs) offer predictability — but at a cost. While some promotional CDs currently reach around 4% APY, those are exceptions. Most CDs average closer to 2–3%, especially once you account for longer terms or non-promotional rates.

That might sound stable, but when you factor in inflation, those returns lose much of their impact. Inflation steadily reduces your purchasing power — meaning the same dollar buys less over time. In fact, over the past 12 months, inflation measured by The Consumer Price Index (CPI) has been about 2.9 %.

So if your CD is earning 4% APY, your real return after inflation is only about 1.1 % (4% − 2.9%). And if your CD yields closer to 3%, the real gain might be near 0.1 % or even negative.

(For those sitting on expiring CDs or low-yield accounts, you might be wondering how to make your money work harder — we cover that next in our article on cashing out of a CD and turning to real estate.)

Real estate offers a more dynamic form of compounding. It grows through both cash flow and appreciation — meaning your returns can build on multiple fronts.

Remember how inflation worked against you with savings or CDs? With real estate, it often does the opposite. Because homes are tangible assets with intrinsic value and real-world utility, their prices tend to rise along with inflation — sometimes even faster. As the cost of goods and materials increases, so does the cost of housing, which naturally lifts property values over time.

Together, these factors create a dual-compounding effect that not only outpaces traditional interest-based accounts but also turns inflation into an ally rather than a threat.

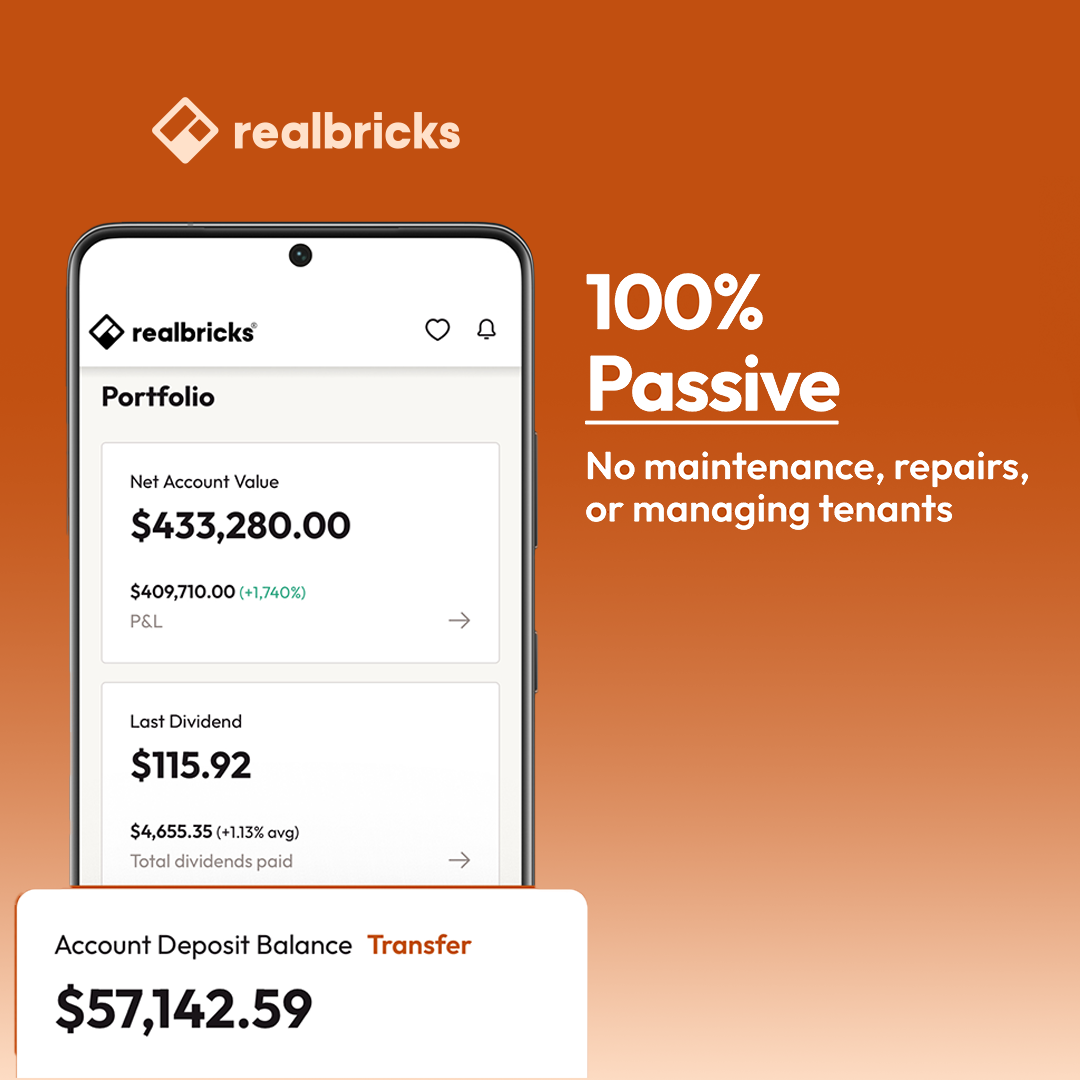

With Realbricks, investors can gain exposure to real estate by purchasing shares of individual properties with a minimum investment of $100. Each share represents an interest in a carefully vetted long-term rental property that has projected dividend distributions from rental income on a quarterly basis and allows investors to gain exposure in changes in property value over time.

By choosing to reinvest distributions, investors may increase their overall exposure to real estate over time. This approach can help build momentum through reinvestment, similar in concept to compounding, while remaining tied to tangible, income-generating assets.

Compounding doesn’t require perfect timing or massive capital — it just takes discipline. Whether you’re building savings or investing in real estate, the earlier you start, the more time your returns have to multiply.

For example, let’s say you invest $100 a month and earn an average annual return of 8%. After 10 years, you’d have around $18,000 — and after 20 years, that amount could grow to over $59,000.

That’s the quiet magic of compound interest: steady contributions over time can create exponential results. When applied to real estate — with both cash flow and appreciation working in your favor — that effect becomes even more powerful.

At Realbricks, investors have experienced an annualized return of roughly 8.25%, with four consecutive quarterly dividends, 2.25% in Q4 2024, 2% in Q1 2025, 2.00% Q2 2025, and 2% in Q3 of 2025, paid from rental income. It’s a tangible example of compounding in action — real assets generating consistent returns, quarter after quarter.

Time can be an important factor in investing. Realbricks allows investors to access real estate assets over time with a low minimum investment of $100.

Disclaimer: Investing in real estate involves risks, including the potential loss of capital. This content is for informational purposes only and is not intended as investment advice. Investors should perform their own research and consult with financial professionals before making investment decisions.

Be the first to know about property launches, portfolio updates, and announcements by subscribing to our newsletter.

Terra Mint Group, Corp ("Terra Mint"), as the Managing Member of Neptune REM, LLC ("Neptune") operates the RealBricks.com website (the "Site") and is not a broker-dealer or investment advisor. All securities related activity is conducted through Dalmore Group LLC, a registered broker-dealer and member of FINRA/SIPC, located at 525 Green Pl. Woodmere, NY 11598. You can review the brokercheck for Dalmore. An up-to-date Dalmore Form CRS is available.

You should speak with your financial advisor, accountant and/or attorney when evaluating any offering. Neither Terra Mint, Neptune, nor Dalmore makes any recommendations or provides advice about investments, and no communication, through this website or in any other medium, should be construed as a recommendation for any security offered on or off this investment platform. The Site may make forward-looking statements. You should not rely on these statements but should carefully evaluate the offering materials in assessing any investment opportunity, including the complete set of risk factors that are provided as part of the offering circular for your consideration.

Neptune is conducting public offerings pursuant to Regulation A, as amended, through the Site. The most current offering circular for Neptune is available here. Past performance is no guarantee of future results. Investments such as those on the Realbricks platform are speculative and involve substantial risks to consider before investing. These risks are outlined in the respective offering materials and including, but not limited to, illiquidity and a complete loss of capital. Key risks include, but are not limited to, limited operating history, reliance on key personnel, inherent risks in investing in real estate, distributions may not be received on predictable schedule and or at all by Investors, and lack of voting rights. Also, the adverse economic effects of the COVID-19 pandemic remain unknown and could materially impact this investment. An investment in an offering constitutes only an investment in a particular series and not in the underlying asset(s). Investors should carefully review the risks located in the respective offering materials for a more comprehensive discussion of risk.

From time to time, Neptune may undertake "testing the waters" for additional series of securities to be offered pursuant to Regulation A. For offerings that have not yet been qualified, no money or other consideration is being solicited, and if sent in response, will not be accepted.

NO MONEY OR OTHER CONSIDERATION IS BEING SOLICITED, AND IF SENT IN RESPONSE, WILL NOT BE ACCEPTED.

NO OFFER TO BUY THE SECURITIES CAN BE ACCEPTED AND NO PART OF THE PURCHASE PRICE CAN BE RECEIVED UNTIL THE OFFERING STATEMENT FILED BY THE COMPANY WITH THE SEC HAS BEEN QUALIFIED BY THE SEC. ANY SUCH OFFER MAY BE WITHDRAWN OR REVOKED, WITHOUT OBLIGATION OR COMMITMENT OF ANY KIND, AT ANY TIME BEFORE NOTICE OF ACCEPTANCE GIVEN AFTER THE DATE OF QUALIFICATION.

AN INDICATION OF INTEREST INVOLVES NO OBLIGATION OR COMMITMENT OF ANY KIND.

AN OFFERING STATEMENT REGARDING THIS OFFERING HAS BEEN FILED WITH THE SEC. YOU MAY OBTAIN A COPY OF THE PRELIMINARY OFFERING CIRCULAR THAT IS PART OF THAT OFFERING STATEMENT FROM: Neptune REM, LLC 412 W Norfolk Ave STE 2, Norfolk, NE 68701 OR HERE.

Investment overviews contained herein contain summaries of the purpose and the principal business terms of the investment opportunities. Such summaries are intended for informational purposes only and do not purport to be complete, and each is qualified in its entirety by reference to the more-detailed discussions contained in the respective offering circular filed with the SEC.

Realbricks does not offer refunds after an investment has been made. Please review the relevant offering materials and subscription documentation for more information.

Potential investors should not rely on any forward-looking statements regarding any investment opportunity, which is based on our beliefs and information currently available to us. The words “anticipate,” “believe,” “expect,” “aim,” “potential,” “design,” “target,” “intend,” “may,” “might,” “plan,” “estimate,” “project,” “projection,” “should,” “will,” “would,” “result” and similar expressions identify forward-looking statements. Such statements are subject to risks, uncertainties, and assumptions and are not guarantees of future performance, which may be affected by known and unknown risks, trends, uncertainties, and factors that are beyond our control. These risks could result in the loss of your investment. See the offering materials for detailed information.

Neptune does not have a public trading market for its Series Interests. While it intends to seek a quotation on PPEX, an alternative trading system (ATS) operated by North Capital Investment Technology, Inc. (“PPEX”) with a view to providing our holders of Series Interests with potential liquidity in the form of a secondary market for their investment in our Series Interests. However, there can be no guarantee that a secondary market may develop, or if it does, as to the volume or pricing with respect to any secondary trading that might develop. The PPEX does not employ market makers to provide liquidity, unlike national securities exchanges. Until Neptune’s Series Interests are listed, if ever, you may not sell the company’s Series Interests. Therefore, it may be difficult for you to sell Neptune’s Series Interests at the time you wish to do so, if you are able to sell them at all. If you are able to sell your Series Interests, you may have to sell them at a substantial discount to their public offering price. Because of the illiquid nature of our Series Interests, you should purchase Neptune’s Series Interests only as a long-term investment and be prepared to hold them for an indefinite period of time.

Property information shown has been provided from various sources, which can include the seller and/or public records. It is believed reliable but not guaranteed and should not be relied upon without independent verification.

Disclaimer: Images, Information and Floor Plan and Measurements are approximate and are for illustrative purposes only. We make no guarantee, warranty or representation as to the accuracy and completeness of the floor plans, measurements and or any information provided. You or your advisers should conduct a careful, independent investigation of the property to determine to your satisfaction as to the suitability of the property for your space requirements. All pricing and availability is subject to change. The information is to be used as a point of reference and not a binding agreement.